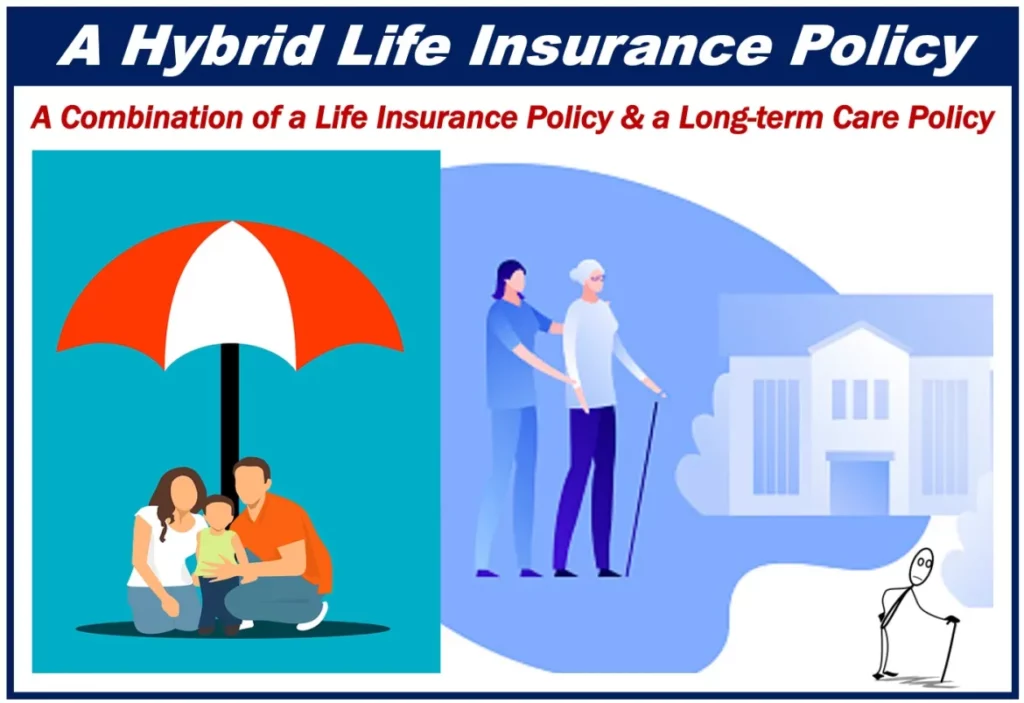

Hybrid Term Life Policy

Hybrid term life cover is more than a scam. However, it is an excellent choice for people who need a term life cover that combines the benefits of term life cover and income protection insurance at the same time.

Suppose someone says, “I offer a hybrid of both.” In that case, they are speaking the truth, as it is exceptionally difficult to find any policy that combines term life cover and income protection insurance at the same time.

It is a very good choice for people who need life insurance but do not want to pay premiums as they are actively living on wages.

This is because when you purchase hybrid term life cover, you will be paying a fixed premium which means that it is much cheaper than a policy with both term life cover and income protection insurance at the same time, even though you only need one policy to cover your entire life.

FAQs on Hybrid Term Life Policy

Q)- What will a hybrid term life insurance product do for me?

Answer)- When you purchase hybrid term life insurance, it is designed to be an excellent choice for people who require quite good protection when they are old but who also need a flexible policy to cover the cost of their child’s education.

Q)- What benefits can I expect from my hybrid term life insurance policy?

Answer]- The main benefit of a hybrid term life insurance is that it provides good protection for the old, and it can also be a very cheap option that can help you save money and give you peace of mind.

Q)- What is the most important thing to consider when buying hybrid term life insurance?

Answer]- The main thing you should pay attention to when choosing a product is the price. The cheapest way to buy a product that is not really of good quality is that you will have to pay quite a lot more than if you would buy it at the best price.

Q)- Can I know if I can afford hybrid term life insurance without covering my child’s education?

Answer]- The answer is yes, it is possible to afford the product without covering your child’s education. However, the most important thing is to buy it wisely and only when you have enough money to cover your needs.

Q)- What are the main benefits of hybrid term life insurance?

Answer]- The main benefit of a hybrid term life insurance is that it provides good protection for the old. This means that you will have more peace of mind when your child deals with a financial crisis.

Q)- What are the main disadvantages of hybrid term life insurance?

Answer]- The main disadvantage of a hybrid term life insurance is that it does not provide as much protection for your child, especially if they do something bad, such as drinking or taking drugs.

Q)- How do I purchase a hybrid term life insurance?

Answer]- The best way to purchase a product such as a hybrid term life insurance is to use the internet. You can get information on how much you need to pay, the year of purchase, and the amount of cover. You will also find out when you can take out your policy and take out your policy.

Q)- What are the different types of hybrid term life insurance?

Answer]- There is a wide range of products available for hybrid term life insurance.

These products include:

A) Single premium option –

This type of product will give you the right amount of protection provided that you make payments on time every month.

B) Multi premium –

This product will give you the right amount of protection, up to the maximum limit. You can assess when you have paid for your policy and decide whether or not to renew it.

C) Term life insurance –

This product is available only for a set period, and it also covers the whole year so that there are no gaps in coverage.

Q)- What are your comments on the new pricing guidelines for term policies?

Answer]- BCBS has put together the revised policy pricing guidelines, announced at a press conference on 7th March 2017. They will be implemented from 1st April 2017.

Q)- How will the new policy pricing guidelines impact the premium I pay for my term life insurance?

Answer]- The new policy pricing guidelines will affect all policies, and it is expected that most of them will now go up by around 1% to 3%. The average increase for a term life insurance policy is 5.5% compared with 4. .9% in 2016.